THE WEEK AMERICAN TURNED BLOCKCHAIN INTO FINANCIAL INFRASTRUCTURE

Three regulatory events. One week. The most consequential restructuring of financial infrastructure since the internet.

Something happened this week that most financial media dressed up as a niche policy story.

It isn’t.

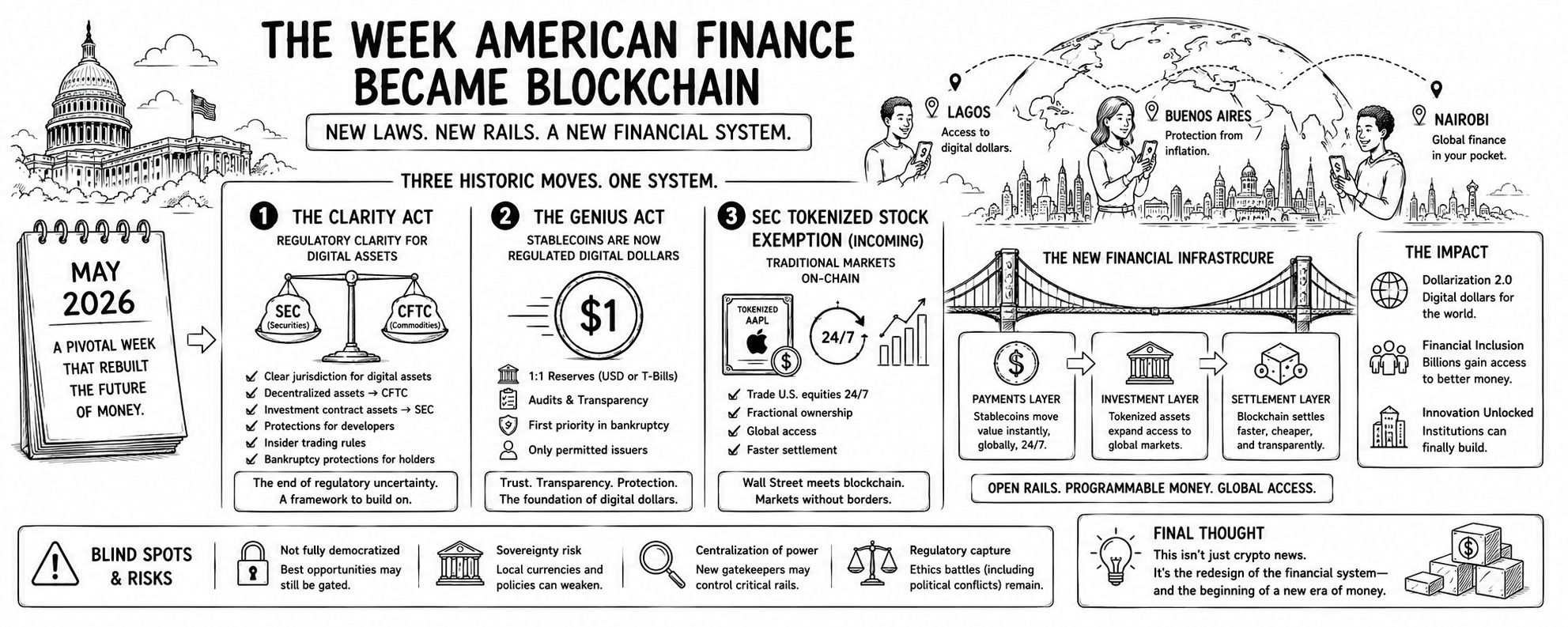

What happened this week quietly, almost bureaucratically is that the United States completed the first real regulatory architecture for digital money since the invention of the internet. Not a trial run. Not a sandbox experiment. An actual, enforceable, bipartisan legal framework that tells every bank, every fund manager, every government, and every curious person in Lagos or Buenos Aires: *this is real now.*

Three things landed inside one week. Three things that individually would be big news together, they are the story of how 2026 becomes the year money changed shape permanently.

Let’s break all of it down. No jargon left unexplained. No shortcuts.

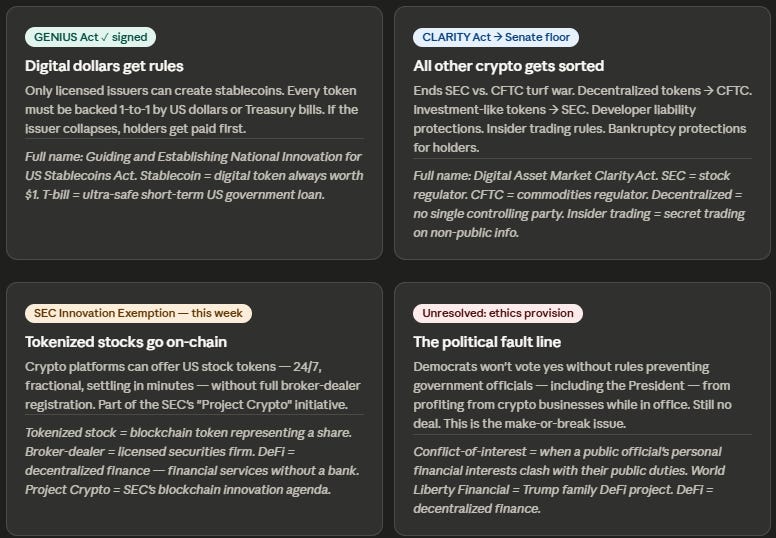

The CLARITY Act Just Cleared Its Biggest Hurdle

On May 14, 2026, the U.S. Senate Banking Committee voted 15-9 to advance the **CLARITY Act** short for the **Digital Asset Market Clarity Act** the most comprehensive crypto legislation ever drafted in the United States.

Let’s be precise about what “cleared committee” means, because the headlines made it sound like it became law. It didn’t not yet. But this was the hardest gate to pass. Think of it like a bill passing its most grueling university entrance exam. It still needs to pass the full Senate (all 100 senators, needing 60 “yes” votes to avoid being blocked), reconcile with the House version, and get the President’s signature. The White House has already flagged July 4th as a target signing date.

“So what does the CLARITY Act actually do?”

Here’s the simplest version:

For years, two regulators in the US have been fighting over who’s in charge of crypto and that fight cost the industry billions in legal fees, drove talent overseas and left regular investors completely unprotected.

The two regulators are:

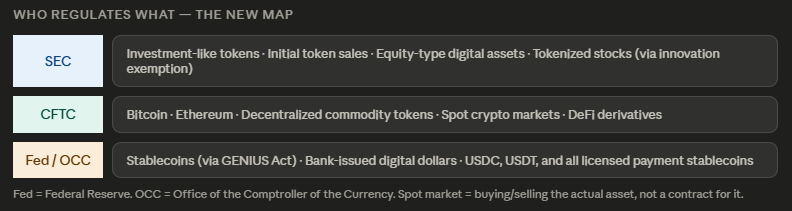

The SEC: the “Securities and Exchange Commission” which oversees stocks, bonds, and financial instruments that represent a share of ownership or a promise of future profits. Think of the SEC as the referee of Wall Street.

The CFTC: the “Commodity Futures Trading Commission” which oversees raw materials and commodities like oil, gold and agricultural goods. Think of the CFTC as the referee of the Chicago trading pits.

Bitcoin looked like a commodity. Ethereum looked like something in between. Most other tokens looked like securities. Nobody agreed. Both regulators kept suing crypto companies claiming jurisdiction. Companies didn’t know which rules to follow. So they either hired armies of lawyers or moved to Dubai, Singapore, and the Cayman Islands.

The CLARITY Act ends this standoff.

It creates a clear sorting system: if your digital asset is “decentralized” (meaning no single company or person controls it), it’s treated as a *”digital commodity” under the CFTC’s watch. If it’s more centralized, more like a company raising money from investors, it’s treated as an “investment contract asset” under the SEC. Everything has a lane. Everyone knows the rules.

The bill also includes protections for “software developers” meaning the programmer who wrote the code that a criminal later misused can’t be held liable for that crime. It adds rules on “insider trading” (someone at a crypto company secretly trading on information before it’s public now explicitly illegal). And it creates new “bankruptcy protections” for people who hold digital assets meaning if the exchange holding your crypto collapses, you’re first in line to get your money back, not last.

The part nobody is talking about: the ethics provision fight.

The most contentious unresolved issue isn’t about crypto at all it’s about whether the law should prohibit government officials, including the President, from personally profiting from crypto businesses while in office. President Trump’s family has significant crypto interests including a meme coin, a DeFi (decentralized finance software-based financial services with no bank in the middle) project called “World Liberty Financial”, and a mining company. Democrats say no ethics provision, no deal. The White House said no rule that targets the President specifically. Senators Ruben Gallego and Angela Also brooks the two Democrats who voted yes in committee said clearly their floor votes depend on this being resolved. Prediction markets (“Polymarket” an online platform where people bet real money on real-world outcomes) moved the odds of the CLARITY Act being signed into law in 2026 from the low 60s to 73% after the committee vote. That’s meaningful.

Why this matters to you even if you’ve never bought a single dollar of crypto:

Because the CLARITY Act isn’t just about crypto companies. It’s about whether the next generation of financial infrastructure gets built in the US or somewhere else. Every major bank, pension fund, and asset manager has been waiting on this legislation before deploying serious capital into digital asset markets. When the rules become clear, the money moves.

The GENIUS Act Already Passed. Here’s What It Did(Recap)

Before the CLARITY Act, there was the GENIUS Act short for the “Guiding and Establishing National Innovation for US Stablecoins Act”. Signed into law by President Trump on July 18, 2025. This one is already done. Already real.

What is a stablecoin?

A stablecoin is a digital token designed to always be worth exactly $1. Not $1.20 one day and $0.60 the next like Bitcoin exactly $1, always, by design. The most widely used ones are USDC (USD Coin, issued by a company called Circle) and USDT (Tether). Combined, stablecoins now represent a market of over $230 billion and their transaction volume in 2024 already surpassed that of Visa and Mastercard combined. Read that sentence again. The pipes that move digital dollars processed more money than the two biggest card networks on Earth.

What the GENIUS Act did:

Before this law, anyone could theoretically issue a stablecoin. After it, only “permitted issuers” can meaning either a subsidiary of a federally insured bank, a licensed non-bank issuer approved by the federal government, or a state-licensed issuer (with limits). Every permitted issuer must:

- Hold “reserves” real US dollars or short-term US Treasury bills (T-bills": ultra-safe short-term loans to the US government) equal to every stablecoin they’ve issued, one-to-one. If you have 100 USDC tokens in your wallet, someone is holding exactly $100 in cash or equivalent somewhere, ready to give back to you.

- Submit to regular audits and transparency reports.

- Give holders “first priority” in any bankruptcy: meaning if the issuer collapses, you get paid before anyone else.

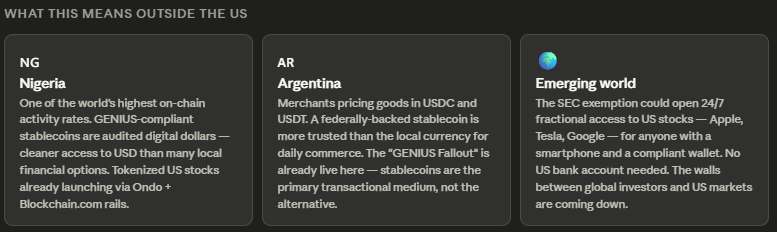

For someone in Nigeria, Argentina, Turkey, or any country where the local currency is eroding a GENIUS-compliant stablecoin is now the most trusted digital dollar they’ve ever had access to. Not because of marketing. Because of US federal law.

“The GENIUS Act and CLARITY Act are two halves of one system.” The GENIUS Act governs the *money* (stablecoins). The CLARITY Act governs the *markets* (everything else). Together, they are the first complete federal framework for digital finance.

The SEC’s Bombshell: Tokenized Stocks Are About to Trade On-Chain

This one arrived this week and barely made the front page.

The “SEC” remember, the stock market regulator is expected to release an “innovation exemption” for “tokenized stocks” as early as May 18, 2026, under “SEC Chair Paul Atkins”.

What is a tokenized stock?

Imagine you want to own a share of Apple (AAPL). Normally, you’d need a brokerage account, US banking access, and you’d wait until US market hours (9:30 AM to 4 PM New York time, Monday through Friday) to trade it. A tokenized stock is a blockchain-based representation of that same Apple share tradable 24 hours a day, 7 days a week, from any device, settled in minutes instead of days, with the possibility of fractional ownership (you can buy $5 worth instead of one full share at $200).

What the SEC innovation exemption means:

Until now, offering tokenized stocks in the US required full “broker-dealer registration” an expensive, time-consuming process that locked out most crypto-native platforms. The exemption would allow platforms like Coinbase (one of the largest US crypto exchanges) to offer tokenized stock trading without going through the full registration process, under specific guardrails exposure limits, disclosure requirements, and a temporary experimental status.

Here’s the quietly controversial part: the framework reportedly includes :third-party tokenized securities” meaning tokens that represent a stock’s price and performance, even without the underlying company’s explicit approval. So a platform could theoretically offer you a “tokenized Tesla” token without Tesla having agreed to it. The token tracks Tesla’s price, but doesn’t necessarily come with voting rights or dividends.

This is where the tension sits. Traditional financial institutions **SIFMA** (the Securities Industry and Financial Markets Association the main lobbying body for Wall Street firms) and Citadel Securities have raised concerns that broad exemptions could weaken **KYC** (Know Your Customer rules that require financial institutions to verify who they’re doing business with) and **AML** (Anti-Money Laundering rules to prevent illegal funds from being laundered through financial systems) controls.

This is a live, developing story. The exemption is part of the SEC’s broader initiative called “Project Crypto” a directive under Atkins to reposition the SEC as a facilitator of financial innovation rather than its primary obstacle.

The Nasdaq and NYSE the two largest stock exchanges in the world have already received approval to list tokenized versions of select stocks. The SEC exemption would extend that infrastructure to crypto-native platforms and DeFi protocols.

“For the emerging world, this is significant in a different way entirely.”

There are over 20,000 publicly listed companies across emerging markets. US investors can access less than 2% of them through domestic exchanges. Meanwhile, a retail investor in India cannot easily access Apple stock. Someone in Nigeria can’t simply open a TD Ameritrade account. Tokenized stocks issued through compliant, regulated frameworks begin to dissolve those walls. Ondo Finance and Blockchain.com already partnered in 2025 to launch tokenized US equities for retail investors in Nigeria. The SEC exemption is the regulatory green light that makes that model mainstream, not experimental.

The Sidebar Stories You Should Know

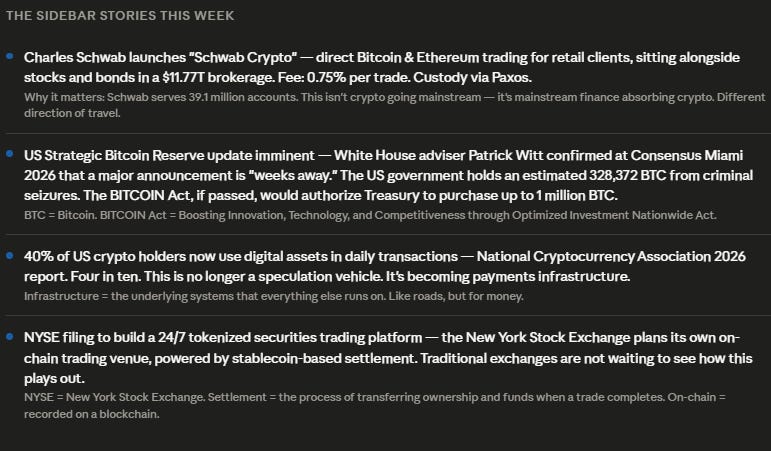

Charles Schwab just launched spot crypto trading for retail clients."

Schwab :— a brokerage firm managing $11.77 trillion in client assets and serving 39.1 million active accounts launched “Schwab Crypto” this week, allowing direct Bitcoin and Ethereum trading for retail clients alongside their stocks and bonds. The platform uses **Paxos** (a regulated blockchain infrastructure provider) for trade execution and **sub-custody** (holding assets on behalf of clients underneath Schwab’s brand). The fee is 75 basis points per trade (0.75%).

Why does this matter? Because Schwab is not a crypto company. Schwab is the financial institution where millions of American retirees, parents, and long-term savers hold their life savings. When Schwab builds a Bitcoin on-ramp, it doesn’t move crypto toward mainstream finance. It moves mainstream finance into crypto. That’s a different direction of travel than most people realize.

The US Strategic Bitcoin Reserve is about to get its first real public update.

In March 2025, Trump signed an executive order establishing the "“Strategic Bitcoin Reserve” a government-held stockpile of Bitcoin funded entirely by seized assets (Bitcoin confiscated from criminals through court proceedings). The US government currently holds an estimated 328,372 BTC. White House crypto adviser Patrick Witt told the Consensus Miami 2026 conference that an official update on the reserve is coming “in the next few weeks.” He declined to confirm the exact size of current holdings but said the priority is to “get our own house in order” before going public. If the “BITCOIN Act” : legislation that would formally codify the reserve and authorize Treasury to purchase up to 1 million BTC passes Congress, the Treasury could begin its first official open-market Bitcoin purchase in Q4 2026. That would make the United States the first sovereign nation to actively buy Bitcoin as a reserve asset.

“40% of US crypto holders now use it in daily transactions” according to the National Cryptocurrency Association’s 2026 report. Four in ten. This is no longer an investment product being held and waited on. It’s becoming infrastructure.

The Part Nobody Wants to Say Out Loud

Here’s the thing that should make you stop and think, regardless of whether you own a single satoshi (the smallest unit of Bitcoin one hundred millionth of one BTC):

The financial architecture being built right now stablecoin rails under the GENIUS Act, market structure under the CLARITY Act, tokenized equity through the SEC exemption is not being built *for* crypto enthusiasts.

It’s being built for the same reason countries build roads. Not so that Formula 1 drivers can race. So that goods can move. So that people can get to work.

The blockchain is becoming infrastructure. Not metaphor. Infrastructure.

And the people who benefit most from infrastructure are rarely the ones who understand how it works. They’re the ones who need it the merchant in Benin City pricing goods in a currency that doesn’t lose 30% of its value by year-end. The first-generation university student who needs to send money home without losing 8% to remittance fees. The farmer in Kenya who wants exposure to global equity markets without flying to New York.

The regulatory stack being assembled in Washington right now is not primarily a gift to Coinbase, Ripple, or any other company that lobbied for it. It’s a redesign of the rails that global value runs on. And for the first time, those rails are being built to be open.

*Sources: CoinDesk, CNBC, The Block, DeFi Rate, Coinpaprika, CryptoTimes, BitBo, BeInCrypto, The Street Crypto, Latham & Watkins US Crypto Policy Tracker, K&L Gates, CoinGecko RWA Report 2026, Charles Schwab 10-Q Q1 2026, Congress.gov, Wikipedia Strategic Bitcoin Reserve, Cornell Emerging Markets Institute 2025. Data accurate as of May 19, 2026.*

© [Easy Weezy From EasyRococo📈] 2026

“If you find such topics interesting And enjoy reading my post, feel free to support my work by buying me coffee or upgrading to paid subscription thank you for your support, bye for now”

Ohhhhh goodness then I really gave thought to the name of your publication, Easy Weezy. I believe I will get through the lessons in a wheef, like a walk in the park on a summer morning. Thanks again. We definitely will keep in touch

I tried to read but I must admit I need lessons on it all 🤣🤣🤣🤣 you got a beginner learner here. They say you're never too old to learn new things.